MIND. The Insurance Game, Explained.

It is an interesting system we have created in the health care world. Broken, many say. Profit driven, some say. Confusing, just about all say. Having experienced both ends as both a patient and provider that has taken insurance, I’d like to chime in and pull back the curtain of transparency. And yes - it is a mind game, and one it seems very few can win. If you’re curious about the seemingly mundane but perhaps eye-opening logistics of health insurance ($3.6 trillion annual spend) and health care ($5.3 trillion annual, or 18% of the GDP), read on. I’ll break down three main points that you may not know about the behind the scenes world of health insurance.

First, reimbursement amount and timing is very unpredictable. When I began practice, I took every insurance that accepted me. [An aside, that medicaid, VA and most medicare plans do not cover naturopathic care.] My initial observation as a new grad desperate for income flow was, jeez, some insurance payers really take their sweet time. As a matter of fact, I still have some from 2023-2025 (over 100, last I checked) that aren’t paid out, and there’s low hope for remittance at this point. Just consider it pro bono, without my patient likely knowing or realizing.

As a provider that focuses on quality and usually a longer visit, over a mentality of quantity and “see 20 per day” model, this made my monthly income wildly unpredictable. I soon realized I didn’t know what I get paid for whom, and when - so I began tracking through a de-identified excel spreadsheet, now with over 1350 unique visits (more on this later). It’s not easy or straightforward to track if a payment is outstanding, or what the actual cumulative reimbursement is between co-pay, insurance payout, and patient deductible.

Second, insurance pays what they want, and the requesting side (providers, hospital systems) aren’t able to request for the remaining difference. Think of it this way: imagine if you were a landlord, and your tenets paid you on their own timeline, and also the amount they deem necessary for rent - and you can’t bargain with them.

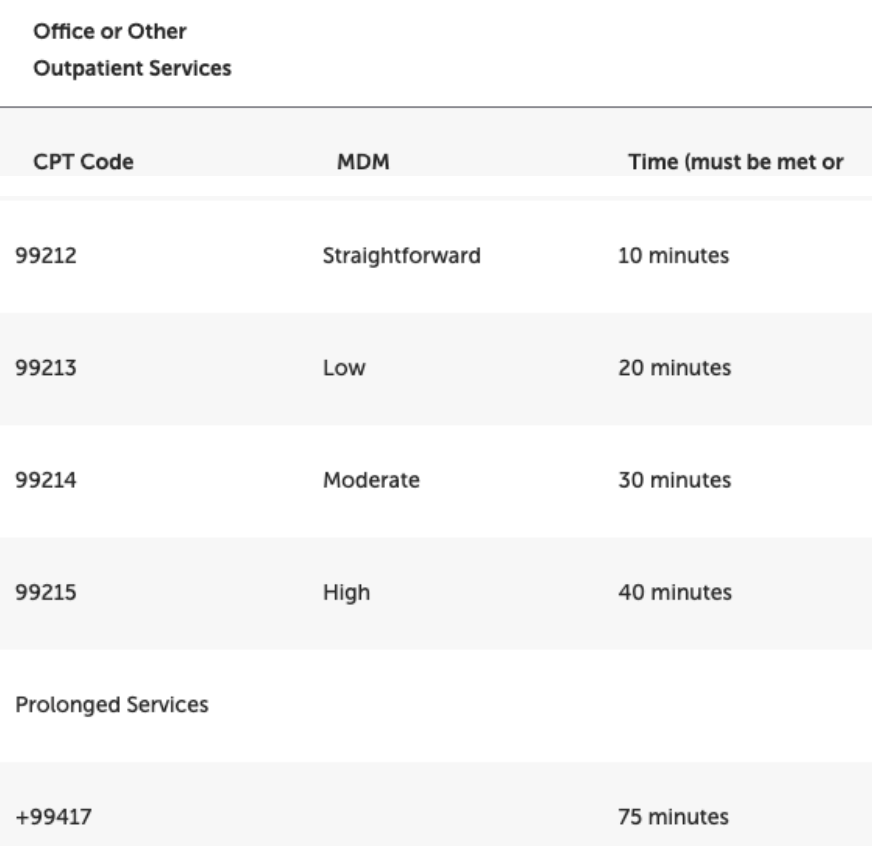

I may be getting too technical, but I really do think it is important for people to know what and how they are being charged, and how their doctor is being paid. Doctors taking insurance bill out codes based on their time (this recently changed from medical complexity model in 2021). The general codes for visits oriented a problem (ie, I have reflux and need help) are as follows, which includes time preparing (reviewing labs, any “presearch” for a condition), time in the visit itself with the patient, and time after the visit (finishing the chart, reviewing records, putting in new prescriptions or lab orders, calling other providers for coordination, etc.):

Photo Courtesy of American Association of Family Physicians.

For efficiency and number optimization, most hospitals and conventional care models aim for a higher quantity of 99213 visit types. This also makes insurance happy because these visits are overall cheaper. These are the visits I hear people complain about of, “they only let me talk about one thing, but I had other things to address.” It’s not that your conventional PCP does not want to talk about more than one chief complaint - the time limit and tightly packed schedule by management bureaucrats make it not possible.

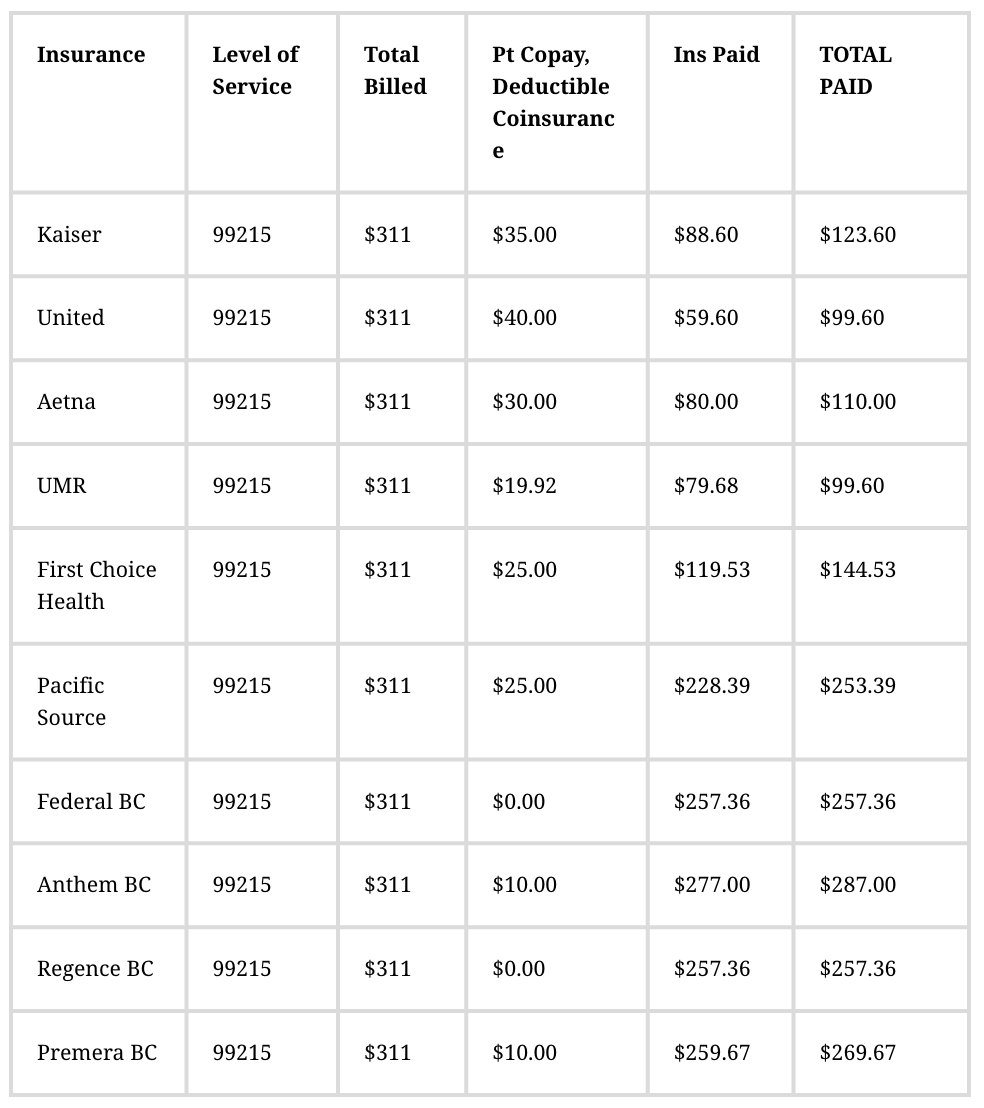

For myself, as an independent contractor, I decided to have most of my visits for 45-minutes in length and generally covered a few to several chief complaints. These visits also usually included checking in and discussions around determinants of health (How are you sleeping now? How are those nutrition changes coming along? How is your support system?) + education around the condition, labs or changes being made. This almost always put into the 99215 category most of the time, and usually much over the 40-minute limit. Our office charged out to insurance $311 for a 99215, less the patient co-pay. See below for the wide variation in what insurance decided to payout - and keep in mind I saw 50-60% of this payout after contributions to the clinic fees:

Created by Dr. Casey Carr with data from real patient visits.

If you are wondering why things cost so much in the insurance and healthcare world, this is why. Hospitals and doctor’s offices will charge high for a service, knowing that insurance will underpay. As discussed, there is no system in place to rebuttal. To add insult to injury, I started to get “threatening” letters from Kaiser, who already underpaid (see above), stating “You bill more 99215s than the average provider - we are keeping an eye on your billing practices.” It caused me such anxiety wondering if I was going to be audited despite diligent charting and recording of time spent, for information to then be skewed and then owe money back to insurance (yes, that happens).

When you take a look at raw cost of service, let’s take the example of a lumbar x-ray (2-3 views). Most medical establishments will bill out to insurance to the tune of $400-$700, in the hopes that they can cover actual cost ($70). If a patient doesn’t have insurance or wants to pay in cash? They are looking at around a reasonable $150.

Which, brings me to my third point… clarity of what insurance covers. If you have a high deductible (aka, a catastrophic plan) insurance plan like myself, your plan covers an annual wellness visit (a code separate from the “complaint-focused” codes, above), but not a lot else. I can’t tell you how many times I had patients come to me after our first visit, a 90-minute comprehensive intake, asking about this bill for $290 they received from the clinic. An annual visit covers only things like reviewing your screening exams due (colonoscopy, DEXA), updating family and personal medical history, and possibly a risk assessment - usually no more than twenty-five minutes. It does not cover specific evaluation and management of complaints. Your insurance won’t cover that, and they likely won’t cover lab work beyond a complete blood count, basic metabolic count, TSH (thyroid) and lipid (cholesterol) panel.

Unfortunately, your healthcare providers are there to provide treatment, not study your insurance plan. It is impossible for the provider to know the nuances of everyone’s individual plan, so it is up to the patient to know what services are covered and what aren’t. I always felt badly when I had patients come to me, frustrated with their bills and coverage. Sometimes half of the visit was spent understanding why their insurance didn’t cover x, y or z - and that is even with an insurance verifier we had on staff to check benefits. You can take every precaution necessary, and even cite the “no surprises act” enacted under Obama - but that still doesn’t mean you won’t like the bill that comes your way.

I’ll give you my own example when I was a patient last year. I enrolled for bronze/catastrophic coverage with Blue Cross. I called them, just I knew I was supposed to, and verified I had an annual wellness visit fully covered under the plan. I decided, heck, I’ll take it, even though I don’t need it! Gain an experience of what a counterpart primary care is doing and how I can improve or change myself. I called the medical office and specified to scheduling I was booking for my annual wellness visit. Great - I was in. I told the front desk when I arrived, here for my annual wellness visit. I told the doctor, yes, I am here for my annual wellness visit and reported zero chief complaints.

Two months later … I receive a bill for $183 and change. I call up the doctor’s office, and their response, “Oh, we don’t do annual wellness visits for the first visit. That’s just to establish care. But you still have your annual wellness visit to use! Would you like to schedule that?” [insert fumes out of my ears here] I call their billing team to debate this issue - I had clearly communicated to all parties involved. After all, I knew the system and took all precautions. I left a message for billing. And another one… and another one. Long story short, I had to physically stop in to the office. According to their office, they weren’t in the wrong, someone surely told me the rule before the appointment. I begrudgingly ended up paying the bill, defeated and frustrated. It gave so much more gusto for the BS that a non-medical person goes through trying to navigate this all. Good luck to all of us.

So, why am I telling you all of this? Number one, I think it is basic education I think most should know who have health insurance. It may be better for you to pay cash for certain services, or maybe now you understand why some visits are just so short. Doctor’s aren’t paid like lawyers, or accountants. Sure, there is an “hourly rate,” but that changes depends on what insurance is paying. And that also doesn’t include the unpaid time of messaging, emergency prescription calls and ER follow-up calls. It makes the whole structure unpredictable and shaky, making bill outs higher to guarantee payment. In this case, shoot for the moon, and you’ll likely still face plant on Earth with this system. And it keeps spiraling to more, and more, and more complexity, expense and frustration.

I am sorry to report that I don’t have a fix for the entire system. But, I am trying on a new type of fix for me: in my new iteration of my new practice, I am not taking insurance. I want cost to be transparent and up front for visits and uncovered labs. I originally thought taking insurance would make me more accessible. And it did, for some. For others, it left them upset, often at me, for the maddening system we call our health care.

Insurance can be ruthless, confusing and downright stingy for many people. For this time period at least, I am taking a break from it all. While I am grateful to have seen and experienced it, my original goal as a naturopathic doctor was to be an alternate in our broken system, and I know feel the freedom that I can really live that out.